April 2, 2025

Why 2025 Is a Prime Year to Invest in Private Real Estate

The private real estate market has faced a challenging cycle over the past two years, with...

Allocating to real estate has always been a bit of a puzzle for investment advisors. From our experience, most will recognize the value of the asset class’s diversification benefits in portfolio construction, however, questions remain about how much to allocate and to which property sectors. Unfortunately, those unknowns can plague many advisors simply because they are not as familiar with commercial real estate as with equities and fixed-income securities.

Still, lack of familiarity has not precluded advisors from participating, as highlighted in a Chatham Partners study.

“A recent study by Chatham Partners found that 83% of financial advisors recommended REITs to their clients. A majority of advisors agree on the underlying long-term fundamentals that support inclusion of REITs within a diversified portfolio.” - reit.com

As you assess your client’s portfolio allocations at the beginning of 2023, you may consider further diversifying your REIT allocation by adding a private real estate sleeve to their portfolios. The vast majority of advisors use publicly-traded REITs, real estate ETFs, and mutual funds to access the asset class, but in doing so, they miss out on other potential benefits non-public securities can offer.

If you have reservations about allocating to alternatives like private equity, real estate, and other illiquid investments, know that advisors, plan sponsors, and institutions alike have turned to private investments to help buffer the impact of a market that saw pullbacks in stocks and bonds in 2022.

“It’s been an unusual market in that both stocks and bonds have gone down together, so it’s been a harsh portfolio market for many investors. The increased interest [in alternatives] reflects an ongoing trend toward the “democratization of alternatives,” - Neil Brown, head of fund investor relations, Actis; planadvisor.com

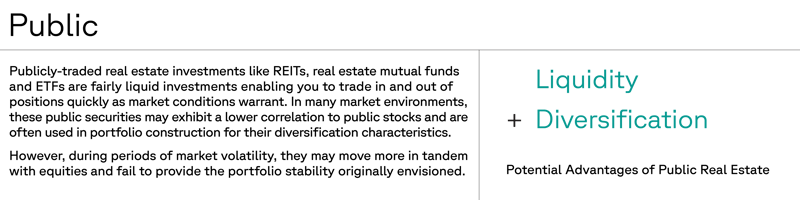

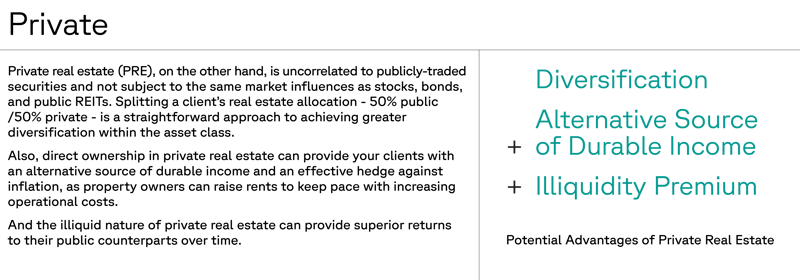

While public and private real estate investments may own similar types of commercial properties, their investment structures can be quite different, as can their respective performance when subjected to different market environments. It’s helpful to understand the potential benefits of each as you evaluate real estate allocations for your clients.

As with any investment, there are risk factors to consider with public REITs and private real estate. Public REIT risks can include market, interest rate, geographic, and concentration risk. Public real estate risks include, liquidity, market, regulatory and credit risk. Carefully assess the risks when considering either of these asset classes.

As with any investment, there are risk factors to consider with public REITs and private real estate. Public REIT risks can include market, interest rate, geographic, and concentration risk. Public real estate risks include, liquidity, market, regulatory and credit risk. Carefully assess the risks when considering either of these asset classes.

As mentioned, the illiquid nature of private real estate may provide enhanced long-term returns compared to publicly traded real estate securities. Also, private real estate’s lower correlation to stocks and bonds than public REITS can offer enhanced diversification characteristics within an overall real estate allocation.

But since public REITs provide investors with liquidity, they can be held for short or extended periods of time with little concern for the need to exit the market during periods of turbulence or when factors turn against specific sectors. In addition, ready access to cash can help investors address any number of cash requirements, including home improvement, college tuition, a family trip, or a new vehicle.

Public REITS can also be used to diversify a portfolio's real estate allocation. For example, an investor may have concentrated private real estate exposure to data centers. Adding several REITs to a portfolio could complement that allocation by providing access to multifamily, retail, and self-storage. And REITs typically have very low investment minimums compared to private investments.

In short, either approach can be a sound portfolio allocation, but combining private real estate and public REITs as a plan for your client’s real estate allocations may offer benefits other advisors are not taking advantage of.

Now is an excellent time to reassess your clients’ real estate allocations. Consider taking some of their market risk associated with public securities off the table by allocating to private real estate.

Important Disclosures:

The information contained in this Presentation is for informational purposes only and is not an offer to sell, or a solicitation of an offer to buy, an interest (“Interest”) in a fund or other investment vehicle (collectively as applicable, a "Fund") by IDR Investment Management, LLC, (“IDR IM”) or their affiliates and subsidiaries.

The information contained herein is subject to change, and may not be reproduced, used or disclosed, in whole or in part, without the prior written consent of IDR-IM.

Statements contained herein are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Firm. Such statements involve known and unknown risks, uncertainties and other factors, and you should not place undue reliance on them. Additionally, “forward-looking statements” may be referenced. Actual events or results or the actual performance may differ materially from those reflected or contemplated in such forward-looking statements.

Certain economic and market information has been obtained from published sources prepared by third parties and in certain cases has not been updated through the date of the Presentation. Neither IDR-IM nor their respective affiliates nor any of their respective employees or agents assumes any responsibility for the accuracy or completeness of such information. The IDR Entities have not made any representation or warranty, express or implied, with respect to the fairness, correctness, accuracy, reasonableness or completeness of any of the information contained herein (including but not limited to information obtained from third parties), and they expressly disclaim any responsibility or liability for this information. IDR-IM and the IDR Entities do not have any responsibility to update or correct any of the information provided herein.

April 2, 2025

The private real estate market has faced a challenging cycle over the past two years, with...

March 12, 2025

Most investment managers have their own version of a “secret sauce” – a system or process they...