October 17, 2024

Investment Advisers Increasing Allocations to Alternatives

Why Private Real Estate is Leading the Way

Introduction

As the financial world becomes more complex, investment advisers are increasingly looking beyond traditional stock and bond portfolios. Many are exploring alternative investments with private real estate often emerging as the preferred choice, favored for its potential to enhance portfolio diversification, generate income, and provide a hedge against inflation.

In this article, we’ll explore why investment advisers are increasingly turning towards alternatives, with a focus on the growing appeal of private real estate, which is gaining momentum as the third vital pillar to a traditional stock and bond portfolio.

Why Alternatives Are on the Rise

Investment advisers have been gradually increasing allocations to alternatives for years, but the momentum is now undeniable. A CAIS-Mercer survey found that 85% of advisers planned to allocate more to alternative assets in 2024.1 Likewise, iCapital's Financial Adviser Survey reports that 80% of advisers already incorporate alternative investments into client portfolios.2

Why the shift? Traditional markets are volatile, and in uncertain times, many advisers are finding that the old 60/40 stock-bond mix isn’t cutting it. Alternatives, particularly those with low correlations to public markets, offer a way to smooth out returns when stock markets get choppy. Simultaneously, they offer greater portfolio diversification and the potential for enhanced returns with alternative sources of income. What was once seen as a niche approach is now a strategic decision to help clients meet their long-term financial goals.

The Wide World of Alternatives

As an adviser, you have no shortage of options when it comes to alternative asset classes, and each comes with its own set of potential benefits and challenges. Some of the more commonly considered options include:

- Private Equity

- Hedge Funds

- Private Real Estate

- Commodities

- Infrastructure

- Venture Capital

- Private Debt

- Art and Collectibles

- Cryptocurrencies

- Managed Futures

- Farmland and Timberland

- Structured Products

Each of these alternatives provides opportunities for diversification and enhanced returns, but it’s important to keep in mind that many often come with trade-offs, such as illiquidity, lack of transparency, and higher risk.

Why Private Real Estate Is Becoming the Go-To Alternative

Historically, private real estate investments faced similar challenges—lack of liquidity, high investment minimums, and limited access for everyday investors. But recent advancements in technology and product design are making it easier for advisers to integrate private real estate into client portfolios.

Take the Accordant ODCE Index Fund, for example. This publicly traded interval fund provides access to a diversified portfolio of high-quality commercial real estate properties across the U.S. Available on all major custodian platforms, it offers daily purchase options, quarterly redemptions, and transparency—features that are making private real estate more accessible to a broad range of investors.

Private real estate’s growing presence in adviser portfolios is no accident. In fact, 96% of advisers report incorporating real estate into their strategies.3 The asset class’s ability to generate stable income, reduce risk through diversification, and hedge against inflation is making it a staple in many portfolios. As the demand for private real estate grows, so too does the accessibility and variety of investment options available to you and your clients.

How Much Should You Allocate to Private Real Estate?

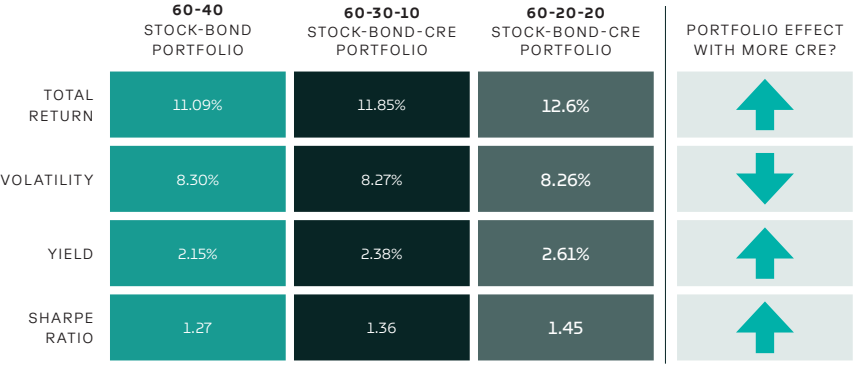

The big question for many advisers is how much to allocate to private real estate. Research shows that adding private commercial real estate (CRE) to a traditional portfolio composed only of stocks and bonds can improve both returns and risk metrics.

For example, portfolios with an allocation to private CRE have historically seen an uplift in yield of over 17% compared to a typical 60/40 stock and bond portfolio.4 More importantly, adding private CRE can increase the portfolio’s Sharpe ratio by approximately 30%, which may lead to a more efficient overall portfolio.

What does this mean in practice? We believe a well-considered allocation of 10-15% to private real estate can potentially offer your clients the diversification and income that suits their investment objectives, particularly in today’s unpredictable market environment.

PORTFOLIO EFFECT BY ADDING CRE - KEY PORTFOLIO STATISTICS

10-YEAR TRAILING PERIOD AS OF 12/31/2023

Source: Affinius Capital Research

(Stocks: S&P 500 Index / Bonds: Bloomberg Aggregate Bond Index /

CRE: NFI-ODCE Index)

What Advisers are Saying

Advisers who have embraced private real estate are seeing positive outcomes, both in portfolio performance and client satisfaction. According to CAIS, many advisers who increased allocations to private real estate have reported higher client satisfaction and better long-term results.5 Escalent's research confirms that the stability and income generation offered by private real estate are top motivators for advisers.6

Looking forward, it’s clear that private real estate is no passing trend. As the market for alternatives grows, it’s likely that more advisers will continue to expand their allocations to this asset class.

Conclusion

The investment landscape is evolving, and so are the strategies needed to help clients achieve their financial goals. Allocating a portion of your clients’ portfolios to private real estate can offer them the diversification, income generation, and inflation protection they need in today’s market.

With research pointing to significant portfolio benefits, now might be the time to consider a 10-15% allocation to private real estate in your clients’ portfolios. And if you’re looking for the latest trends and data on the private CRE market, sign up to our Due Diligence Portal to stay ahead of the curve.

This information is educational in nature and does not constitute a financial promotion, investment advice or an inducement or incitement to participate in any product, offering or investment. Accordant is not adopting, making a recommendation for or endorsing any investment strategy or particular security or property mentioned in this article. All opinions are subject to change without notice, and you should always obtain current information and perform due diligence before participating in any investment. All investing is subject to risk, including the possible loss of principal. Accordant Investments, LLC (“Accordant”) cannot guarantee that the information herein is accurate, complete or timely. Past Performance does not guarantee future results.

Accordant has not made any representation or warranty, express or implied, with respect to the fairness, correctness, accuracy, reasonableness or completeness of any of the information contained herein (including but not limited to information obtained from third parties), and they expressly disclaim any responsibility or liability, therefore Accordant does not have any responsibility to update or correct any of the information provided in this article.

All real estate investments have the potential for value loss during the life of the investment and the sponsor can make no assurances that any investment will achieve its objectives, goals, generate positive returns, or avoid losses.

Investors should carefully consider the investment objectives, risks, charges, and expenses of the Accordant ODCE Index Fund. This and other important information about the Fund is contained in the prospectus, which can be obtained online by visiting www.Accordantinvestments.com The prospectus should be read carefully before investing.

Past Performance is No Guarantee of Future Results.

Investing in the Fund involves risks, including the risk that you may receive little or no return on your investment or that you may lose part or all of your investment. The Fund’s investment objective is to employ an indexing investment approach that seeks to track the NCREIF Fund Index – Open End Diversified Core Equity (the “NFI-ODCE Index”) on a net-of-fee basis while minimizing tracking error. There can be no assurance that the actual allocations will be effective in achieving the Fund’s investment objective or delivering positive returns. It is not possible to invest in an index. You cannot invest directly in an index and unmanaged indices do not reflect fees, expenses, or sales charges.

The ability of the Fund to achieve its investment objective depends, in part, on the ability of the Adviser to allocate effectively the Fund’s assets across the various asset classes in which it invests and to select investments in each such asset class. There can be no assurance that the actual allocations will be effective in achieving the Fund’s investment objective or delivering positive returns. Limited liquidity is provided to shareholders only through the Fund’s quarterly repurchase offers for no less than 5% of the Fund’s shares outstanding at net asset value. There is no guarantee that shareholders will be able to sell all of the shares they desire in a quarterly repurchase offer. The first repurchase offer following the Conversion is expected to occur in February 2024.

Additional risks related to an investment in the Fund are set forth in the “Risk Factors” section of the prospectus, which include, but are not limited to the following: convertible securities risk, correlation risk, credit risk, fixed income risk, leverage risk, and risk of competition between underlying funds.

Investors should consult with their selling agents about the sales load and any additional fees or charges their selling agents might impose on each class of shares.

The Accordant ODCE Index Fund is distributed by ALPS Distributors, Inc (“ALPS”). Accordant Investments LLC is not affiliated with ALPS.

Related Articles

October 22, 2024