Written by: Accordant CFO, Jim Hime

6 min read

Howdy from Dallas, Texas, home of some of the great names in private real estate, such as Crow Holdings and Hillwood Investment Properties.

My name is Jim Hime. I’m the Chief Financial Officer of Accordant Investments, which is a registered investment adviser that advises the Accordant ODCE Index Fund (ODCEX), and I’d like to take this opportunity to tell you a little about my background.

I’ll start with the fact that my wife often says to me, “You’re the Yoda.” I think she is only half-kidding when she does.

Why this imminently practical and level-headed woman, whom I married over fifty years ago, would liken me to an imaginary green creature, smallish in stature, with the pointiest of ears, may or may not become clearer when you read what I’ve written below, in what is the first post launching, in partial homage to Hemingway, “The Old Man and the PRE*” *Private Real Estate, A CFO’s Journal.

This Journal is meant to be about private, institutional-quality real estate (or “PRE” for short), which has only recently become investable as an asset class for people of ordinary walks of life. For many long years before that, stretching way back into the past, it has had a reputation as something reserved for the very largest investors, institutions and really rich people, as well as being a somewhat risky, scary, murky, even dodgy affair.

I have been around PRE since, as the old saying goes, Hector was a pup – almost as long as I’ve been married, in fact. I have seen it evolve from something that was financed mostly by groups of old men gathered at the nineteenth hole of their local country club, on down through the years of institutionalization and globalization, to the data driven, technologically enabled business that it is today.

In these posts, I intend to share some of what I’ve learned, and how my decades of experience shaped my current views on the asset class (including those stories, like the distress that these days afflicts pockets of the office sector, that occasionally make it into the headlines) in hopes of shining a light on what for years has been a rather dark corner of the investment world – because, like Norma Desmond from “Sunsets Boulevard,” it’s PRE is read for its close-up as an asset class, not just for the aristocracy of the investment world, but for thee and me.

Now you may be thinking hang on a minute. What’s up with this adjective “private?” Is there anything more public than a shopping mall, or for that matter an office building or an apartment complex?

Fair point. But when we at Accordant Investments use the phrase “private real estate,” we’re talking not so much about not how it’s used, but instead how it’s financed, that is to say, with private capital in contradistinction to the publicly listed real estate investment trust sector which has historically been the individual investor’s principal way of accessing high quality, institutional assets. As I will come onto in later posts, we draw this distinction because of the meaningful difference in investment performance between private real estate, in the sense in which we use the term, and public REITs.

Now, back to yours truly and how I got here.

Many of you may not realize that, back in the day, before my career even started – back when I was a kid, growing up mostly in small towns in the South –there was barely such a thing as PRE.

Indeed, my first real introduction to PRE, or at least to the kind of asset in which PRE manifested itself, was courtesy of the girl I was dating in 1973 who now joins me in chasing grandkids around on somewhat creaky knees.

I was attending the University of Texas in the summer of ‘73, going to school during the day and making ends meet by working night shifts for minimum wage stocking groceries at an east Austin H-E-B, and living for the weekends when I could drive the three hours to Houston to see my gal. Once we were actually together, since I didn’t have two nickels to rub together, we mostly entertained ourselves by sitting on the couch in her living room enduring the beady-eyed stares of her parents.

One Saturday evening, after suffering through about five minutes of that scrutiny, she turned to me and whispered, “Let’s go to the Galleria.”

“I don’t know what that is,” I whispered back.

“Get your car keys.”

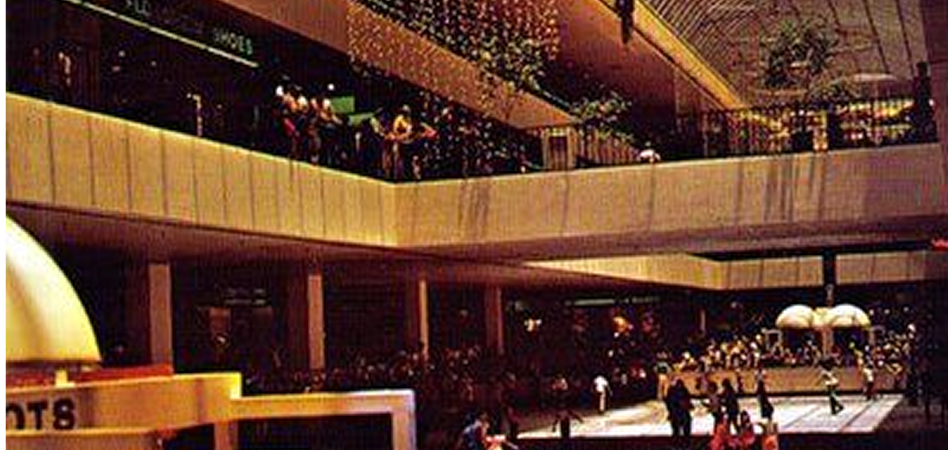

Fifteen minutes later, she was leading her wide-eyed countrified boyfriend by the hand through a three-story enclosed shopping mall that was topped by a glass roof and that had an ice-skating rink on the bottom floor. The department store anchors included Lord & Taylor, Saks Fifth Avenue, and Neiman Marcus. In-line retailers were the likes of Brooks Brothers and Tiffany’s, along with sundry antique stores, card shops and restaurants.

Galleria Mall; Houston, Texas; 1970s

I was agog. I had no idea that such a thing existed or, for that matter, that it could be brought into being by the wit of man.

And I pretty quickly knew that I wanted very much to have something to do with PRE (though I had no notion of the term at the time) during the course of my career, once I had achieved my then dream of graduating from law school.

Graduate I did, in 1976, and joined the Houston-based law firm of Baker & Botts, among whose clients were Gerald D. Hines, developer of the said Galleria and, indeed, of One Shell Plaza, the downtown office building in which Baker & Botts had its blonde-wood paneled offices.

Starting that very year, and continuing to this day, I have had nearly half a century of experience in PRE – first as a tax and deal lawyer, and after twenty years of that, as a senior finance guy for successively, Hines, a small private equity real estate shop, an enormous Middle Eastern sovereign wealth fund, the real estate subsidiary of a well-known US insurance company, and now at Accordant Investments, which I’ll talk at length about in later posts.

I’ve been through at least four booms in PRE, followed by the inevitable four busts, because PRE is nothing if not a cyclical business.

I’m going to say that again:

Private real estate is (ahem, clears throat in order to raise voice) NOTHING IF NOT A CYCLICAL BUSINESS.

Let that be the note on which I close on for now.

In the meantime, just know that good old Yoda here has a lot of wisdom and war stories to share with you, on a weekly or bi-weekly basis or thereabouts (depending on the press of other business/grandkids) so if you’re of a mind to do so, he’d love for you to come along for the ride.

We’ll have ourselves some fun and you might even find some of it sort of interesting, if you or your clients are wondering about whether to add PRE to a portfolio and, if so, how.

As the genuine article himself would say:

Do. Or do not. There is no try.