October 22, 2024

Is Private Real Estate Ready for a Recovery?

Perhaps, but as a strategic investment decision, it shouldn’t matter.

In the world of investing, the notion of timing can often overshadow the more important principle of making strategic decisions. This is particularly true in private real estate, a market characterized by its cyclicality and sheer size. Today, many investors are pondering whether private real estate is poised for a recovery, as many property types have been battered over the past year.

While the answer to that question may lean towards optimism, it's crucial to understand that, as a strategic allocation, the current phase of the real estate cycle should not dictate investment decisions. This article delves into the current cycle, underscores the magnitude and diversity of the private real estate sector, and reaffirms private real estate’s role as a cornerstone of any robust investment portfolio.

Understanding the Private Real Estate Cycle

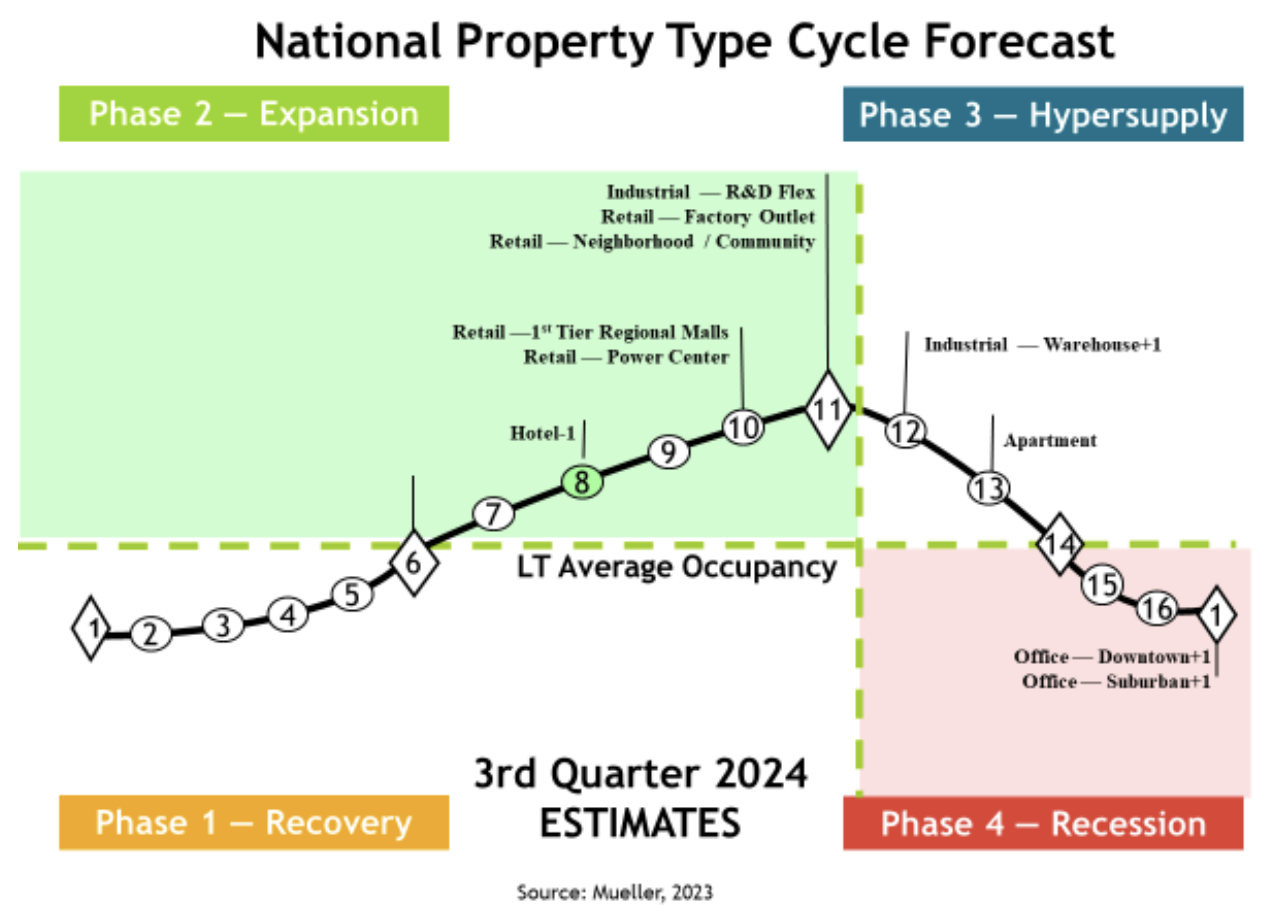

The private real estate cycle is a concept that many investors are familiar with, yet its implications on investment strategy are often overlooked. Considered one of the preeminent specialists on this topic, The University of Denver’s Professor Glen Mueller has meticulously tracked and analyzed the real estate cycle for over thirty years, shedding light on how private real estate performs across sectors, states, and cities through its four distinct phases: recovery, expansion, hyper-supply, and recession. The following chart1 helps illustrate how supply and demand evolve throughout the cycle.

For investors, recognizing that not all private real estate sectors experience the phases of the market cycle at the same time and in the same way, underscores the importance of diversifying across property types and even geographies.

As you’ll note in Mueller’s Q3, 2024 National Property Type Forecast1, few would argue that suburban and downtown office properties don’t belong in the bottom phases of the cycle today. But notice that retail, hotel, and industrial are all in the expansion phase and anticipated to continue to perform well. This disparity in sector performance is another reason why it's difficult to time a recovery.

https://files.secure.website/wscfus/10546084/32174533/cycle-forecast-24q3.pdf

The Size and Diversity of the Private Real Estate Industry

Private real estate is arguably the third largest asset class, behind equities and fixed-income investments. It offers investors the opportunity to diversify their holdings across a range of factors – property type and quality, size, location, investment strategy, manager, and hold period. This diversity not only provides investors with numerous investment opportunities but also, as an asset class uncorrelated to the public markets, may offer a buffer against market volatility. And a well-diversified real estate portfolio helps further mitigate risks compared to a concentrated portfolio.

Beyond buildings and land, private real estate encompasses the economies and communities that it thrives within. As such, the industry's size and significance underscore its resilience and merit as a potential long-term fixture in investors’ portfolios.

Strategic Allocation: A Long-term Perspective

The concept of strategic allocation is central to understanding why current market conditions should not dictate investment decisions in the private real estate sector. Strategic allocation refers to the long-term inclusion of an asset class in an investment portfolio, designed to help achieve diversification and reduce risk over time.

Investors should not be swayed by short-term market trends or attempt to time their entry and exit based on the real estate cycle’s current phase. Instead, emphasis should be placed on the intrinsic value that real estate brings to a portfolio, including its potential for income generation, capital appreciation, and inflation hedging. By adhering to a strategy of long-term allocation, investors can navigate the cyclical nature of the real estate market with confidence, seizing opportunities for growth while mitigating risks.

Conclusion

As we consider the prospect of recovery for private real estate, it's important to remember that the value of this asset class extends beyond its current market phase. Mueller’s Market Cycle Monitor offers compelling evidence that all property types follow their own cycles and that investors could benefit most from remaining steadfast and holding their positions throughout cycles. By prioritizing strategic allocation, investors can help position their real estate investments for long-term success. Ultimately, the resilience of private real estate as an asset class lies not in its immunity to cycles but in the strategic approach investors take towards its inclusion in their portfolios.

This information is educational in nature and does not constitute a financial promotion, investment advice or an inducement or incitement to participate in any product, offering or investment. Accordant is not adopting, making a recommendation for or endorsing any investment strategy or particular security or property mentioned in this article. All opinions are subject to change without notice, and you should always obtain current information and perform due diligence before participating in any investment. All investing is subject to risk, including the possible loss of principal. Accordant Investments, LLC (“Accordant”) cannot guarantee that the information herein is accurate, complete or timely. Past Performance does not guarantee future results.

Accordant has not made any representation or warranty, express or implied, with respect to the fairness, correctness, accuracy, reasonableness or completeness of any of the information contained herein (including but not limited to information obtained from third parties), and they expressly disclaim any responsibility or liability, therefore Accordant does not have any responsibility to update or correct any of the information provided in this article.

All real estate investments have the potential for value loss during the life of the investment and the sponsor can make no assurances that any investment will achieve its objectives, goals, generate positive returns, or avoid losses.